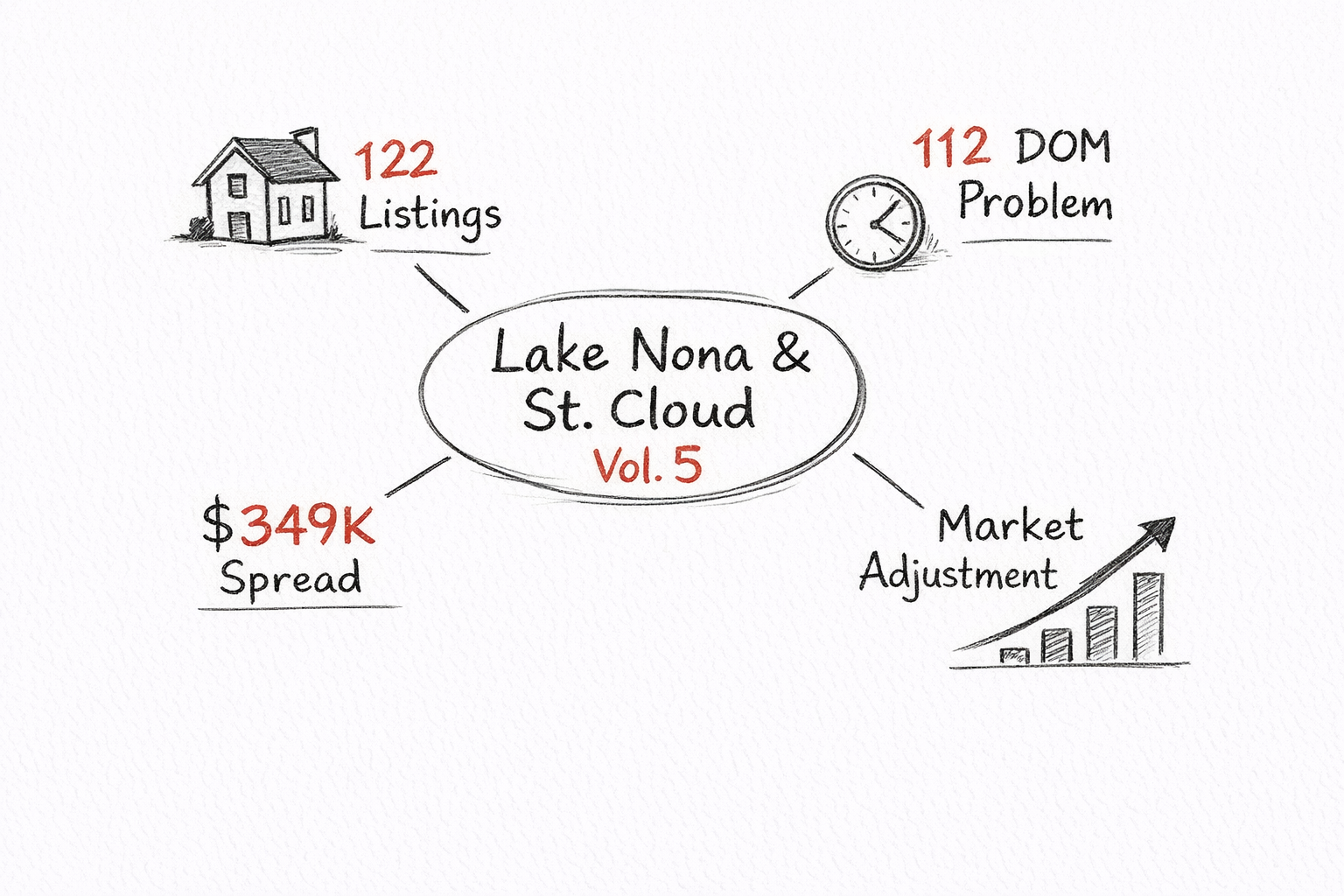

Lake Nona & St. Cloud: The Weekly Market View Vol. 5

Lake Nona & St. Cloud: The Weekly Market View Vol. 5

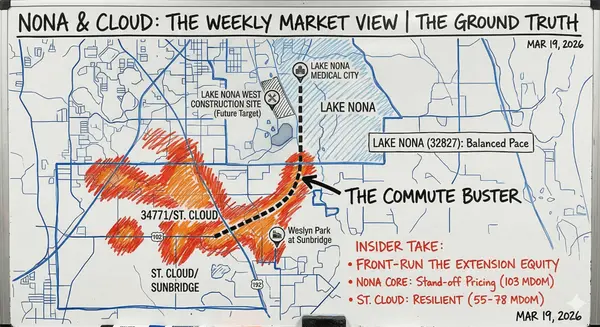

The Inventory Reality Check: Lake Nona Buyers Get More Options, St. Cloud Sellers Face Longer Waits

April's not delivering the development headlines we typically track, but the market data tells a clearer story than any permit filing this week. Lake Nona sits at 122 active listings as of April 15, 2026, with 91 average days on market and a $799,000 median list price. That's the highest April inventory count in recent memory for 32827.

Fifteen miles south, St. Cloud's April median holds steady at $450,000 — flat year-over-year — but days on market stretched to 112. The gap between these two markets isn't just price anymore. It's time to sale.

Lake Nona: The Inventory Inflection

November 2025 saw 83 homes sold in Lake Nona at a $780K median, down 1.3% year-over-year. Fast-forward to April's 122 listings, and you're looking at nearly 50% more available inventory than typical spring levels. That's not a crash — it's an adjustment.

The breakdown shows inventory expansion across price segments. Current median list price sits at $799,000 with an average price per square foot of $460.50. The $500K-$700K range is seeing legitimate inventory expansion for the first time since 2021, while the luxury tier above $1.5M maintains significant available stock.

St. Cloud: The DOM Problem

112 days on market in St. Cloud isn't a seasonal blip — it's the new normal for anything priced above the median. The zip-code story hasn't changed: 34771 still commands the premium, 34769 offers the value play, but everything's taking longer to move.

The zip-level breakdown remains consistent:

- 34771: $464,583 median (northern St. Cloud, Lake Nona adjacent)

- 34769: $322,201 median (central/historic core)

- 34773: $406,504 median (Harmony area)

The $400K+ St. Cloud market is where buyers are getting selective. February 2026 median sale price was $399,440, up 3.5% year-over-year, but that growth rate is decelerating as DOM extends.

The Corridor Arbitrage

The Lake Nona-to-St. Cloud price spread has never been wider in raw dollar terms: $799K vs $450K median list prices creates a $349K gap. But the time arbitrage tells the bigger story.

Lake Nona at 91 DOM vs St. Cloud at 112 DOM means Lake Nona sellers are moving inventory 21 days faster despite being priced 78% higher. That's market efficiency working — Lake Nona buyers know what they're getting and will pay for it when it's priced correctly.

St. Cloud's DOM extension suggests pricing discipline problems. Too many sellers are testing 2022 price memories in a 2026 market.

Strategic Positioning This Week

If you're buying Lake Nona: The expanded inventory is your friend, but it's not creating material price concessions yet. Average homes sell about 3% below list price and go pending in around 57 days. Focus on listings that have been active 60+ days — those sellers are ready to negotiate.

If you're selling Lake Nona: Price to the current 91 DOM, not to last spring's market. The luxury tier ($1M+) is seeing the most inventory pressure. If you're in established neighborhoods under $800K, you're still in the liquid part of the market.

If you're buying St. Cloud: Don't rush. 112 DOM means sellers are adjusting expectations slowly. The 34771/34769 spread offers the best value hunting in 34769 if you're willing to take on renovation projects.

If you're selling St. Cloud: Price 5-7% under comparable recent sales, not recent listings. The DOM penalty for overpricing is real and extending.

Infrastructure Context

The major pipeline projects (Dowden Central CDD, Sunbridge Parkway, SunPark Industrial) remain in development phases without new updates this week. That's fine — the market is digesting the current supply-demand dynamic independent of future infrastructure impacts.

When those projects do accelerate permitting and construction announcements, they'll hit a market that's already in inventory adjustment mode, which should moderate both the supply impact and the pricing volatility.

What We're Watching Next Week

- Lake Nona listing absorption through the remainder of April

- Any DOM improvement in St. Cloud's 34771 premium zip

- New construction delivery schedules from major builders

The development news cycle will resume when it resumes. The market continues regardless.

The Ground Truth Protocol publishes weekly real estate intel every Thursday. For prior volumes and market analysis, visit our archive.

Word count: ~800

NEWSLETTER VERSION

Subject line: Lake Nona hits 122 listings. St. Cloud hits 112 DOM. Here's what breaks first.

The Weekly Market View — Vol. 5

Thursday, April 16, 2026

The week in numbers: Lake Nona inventory expanded to 122 active listings (April 15) with 91 average DOM at $799K median list. St. Cloud holds $450K median but stretched to 112 days on market. The time-to-sale gap is widening faster than the price gap.

Lake Nona's inventory reality: 122 listings is the highest April count in recent memory. Not a crash — an adjustment. The $500K-$700K segment shows the most expansion. The luxury tier ($1M+) maintains significant available stock but isn't moving quickly.

St. Cloud's DOM problem: 112 days isn't seasonal — it's the new normal for anything above median. The zip spread story continues: 34771 at $465K median (Lake Nona adjacent), 34769 at $322K (renovation opportunities), but everything takes longer now.

The corridor math: $799K Lake Nona vs $450K St. Cloud = $349K median spread. But Lake Nona moves in 91 DOM vs St. Cloud's 112 DOM. You're paying 78% more but waiting 21 fewer days. That's market efficiency.

Your moves this week:

Buying Lake Nona: Expanded inventory helps, but no material price concessions yet. Target listings active 60+ days — those sellers will negotiate.

Selling Lake Nona: Price to 91 DOM, not last spring. Luxury tier ($1M+) sees the most inventory pressure.

Buying St. Cloud: Don't rush. 112 DOM means slow seller expectation adjustment. Hunt 34769 if you'll renovate.

Selling St. Cloud: Price 5-7% under recent sales, not recent listings. DOM penalty for overpricing is extending.

Infrastructure watch: Major pipeline projects (Dowden Central, Sunbridge Parkway, SunPark Industrial) remain in development phases. No updates this week. The market's adjusting independent of future supply impacts — which should moderate volatility when those projects do accelerate.

Next week: Watching Lake Nona absorption rates and any St. Cloud DOM improvement in the 34771 premium corridor.

Development news resumes when it resumes. The market continues.

— Chad

Categories

Recent Posts

GET MORE INFORMATION